While the sales volume continues to decline, the median price in this state remains strong. July's median price for single family homes (excluding condominiums) is even a little higher than this time last year, according to the California Association of Realtors.

Partially responsible for this decrease in sales are the tighter lending guidelines--for buyers looking for 100% loans, they are much tougher to find. For all buyers, higher FICO scores are demanded, and some loan programs have disappeared all together. These changes affect the entry level buyers the most, as even a 95% loan-to-value program may be difficult to find.

110 out of 371 communities/cities in this state showed an increase in their median price compared to one year ago. Click on the title link of this article and see the 10 highest priced communities in the state, and the 10 with the greatest increase.

Condos have increased overall to a median price of $434,640, a 2.4% over one year ago.

Real estate is local, so median prices don't reflect changes up or down in other communities on a month-to-month basis.

Important to keep in mind: “It is important to note that decline in sales is not driven by weakening economic conditions ... Rather, the statewide and national economies continue to move forward, with no recession on the horizon at this point in time."

8/22/2007

Vacation or Second Homes

Sometimes, actually a lot of times, people think they don’t have the ability or resources to accomplish a certain goal, and then it truly becomes unattainable. A timely quote for this might be, “People don't plan to fail; they fail to plan.” (This was most recently said by a REALTOR in New Jersey, but don’t think he was the first.)

Sometimes, actually a lot of times, people think they don’t have the ability or resources to accomplish a certain goal, and then it truly becomes unattainable. A timely quote for this might be, “People don't plan to fail; they fail to plan.” (This was most recently said by a REALTOR in New Jersey, but don’t think he was the first.) First, you have to ask yourself what you really want—possibly this will lead to workshops on goal-setting, or minor, then major, soul searching, then therapy. We’ll leave that up to you, but we do recognize that for most people making transitions can take time. Fast forward and move onto your second home strategy.

A down market of new and existing home sales spells opportunity, and the IRS allows for certain benefits, if you plan well. Do you plan to make it your future retirement home? Then area will be especially critical. Have you factored in your upkeep and expenses for maintaining a second home vs. an annual summer rental? Are you living in the desert and wishing for ocean breezes—if you’re calling on a coastal listing and it’s 108 degrees where you live now, you might be calling out of desperation (see “Fools Rush In” at the link) rather than a good long-term plan.

Have you talked with your tax accountant or attorney first to be aware of how you can gain or lose with the IRS—how many days you may or may not rent out the second home, how to avoid the Alternative Minimum Tax or minimize it, or how your Subchapter S corporation through your business can benefit you. Have you thought about your 1031 exchange and capital gains factors if you decide to turn this into an investment property, or vice-versa? If you have an vacation investment property you may be able to exchange it or convert it later to personal use:

A down market of new and existing home sales spells opportunity, and the IRS allows for certain benefits, if you plan well. Do you plan to make it your future retirement home? Then area will be especially critical. Have you factored in your upkeep and expenses for maintaining a second home vs. an annual summer rental? Are you living in the desert and wishing for ocean breezes—if you’re calling on a coastal listing and it’s 108 degrees where you live now, you might be calling out of desperation (see “Fools Rush In” at the link) rather than a good long-term plan.

Have you talked with your tax accountant or attorney first to be aware of how you can gain or lose with the IRS—how many days you may or may not rent out the second home, how to avoid the Alternative Minimum Tax or minimize it, or how your Subchapter S corporation through your business can benefit you. Have you thought about your 1031 exchange and capital gains factors if you decide to turn this into an investment property, or vice-versa? If you have an vacation investment property you may be able to exchange it or convert it later to personal use:

“A section 1031 exchange lets you sell one investment property and defer the capital gains if you put the proceeds into another. You'll have to rent out that new property, too, to qualify for the tax deferral. But after renting the property out for a year, you can convert it back to personal use. There's still no tax until you sell.” (Jeffrey Schnepper is a New Jersey lawyer and CPA, personal finance columnist and the author of several books on tax strategies.)

You could be considering a family home, a smaller cabin, a condo or townhome or a duplex or a triplex near the beach where you could be gaining income on the other units. The initial planning stages may put you through some work, but it’s better than buying a property and later losing money on it because you bought it in that dream like state while you were on vacation already.

You could be considering a family home, a smaller cabin, a condo or townhome or a duplex or a triplex near the beach where you could be gaining income on the other units. The initial planning stages may put you through some work, but it’s better than buying a property and later losing money on it because you bought it in that dream like state while you were on vacation already.

8/14/2007

Not All Pricing Trends Are Down ...

. . . in fact, some are up. Writer Kenneth Harney, based in Washington D.C., reported August 12 about median price increases in Chevy Chase-Bethesda areas, by zip code.

In today's Los Angeles Times, a convenient interactive zip code finder is an interesting feature for finding median prices comparing July 2007 to July 2006. For instance, 90803, a Long Beach area of affluence, ocean views, and mixed single family residences, residential units, and condos, adjacent to the shoreline and a few blocks in, shows a median price increase from under $1,000,000 last year to over $1,000,000 this year, and an increase in the number of sales as well. Go to nearby zip code 90815, an area of mostly single family homes near a shopping center, schools and local libraries, and see the price and number of sales change upward only slightly since last year. On the other hand, Cerritos zip code 90703 has seen an 11% decrease in number of sales with a 3% median price decrease from $690,000 to $668,000 this year.

North Long Beach area 90805 has an 11% decrease in price and an almost 40% decrease in number of sales. This would be more the land of opportunity for the right buyer in the $400,000 price range for a house.

You may find, however, that data is different depending on which source you use: See the zip code chart published in Sunday editions of the Los Angeles Times.

While certain areas are more connected to subprime loans than others, an area of affluence is still not totally immune, since some borrowers stretched themselves to the limit to get into their new home of choice.

According to the Los Angeles Times article using data from Dataquick, "Los Angeles County's median price rose 5.3%, to $547,000, and sales slid 23%, and Orange County's median was flat at $640,000, as sales fell 19.8%."

Long Beach

Long Beach  los angeles county

los angeles county

In today's Los Angeles Times, a convenient interactive zip code finder is an interesting feature for finding median prices comparing July 2007 to July 2006. For instance, 90803, a Long Beach area of affluence, ocean views, and mixed single family residences, residential units, and condos, adjacent to the shoreline and a few blocks in, shows a median price increase from under $1,000,000 last year to over $1,000,000 this year, and an increase in the number of sales as well. Go to nearby zip code 90815, an area of mostly single family homes near a shopping center, schools and local libraries, and see the price and number of sales change upward only slightly since last year. On the other hand, Cerritos zip code 90703 has seen an 11% decrease in number of sales with a 3% median price decrease from $690,000 to $668,000 this year.

North Long Beach area 90805 has an 11% decrease in price and an almost 40% decrease in number of sales. This would be more the land of opportunity for the right buyer in the $400,000 price range for a house.

You may find, however, that data is different depending on which source you use: See the zip code chart published in Sunday editions of the Los Angeles Times.

While certain areas are more connected to subprime loans than others, an area of affluence is still not totally immune, since some borrowers stretched themselves to the limit to get into their new home of choice.

According to the Los Angeles Times article using data from Dataquick, "Los Angeles County's median price rose 5.3%, to $547,000, and sales slid 23%, and Orange County's median was flat at $640,000, as sales fell 19.8%."

Long Beach los angeles county

8/12/2007

Volatility in the Credit Markets

The world of loans and finance is like a global pile of pick-up-sticks, and this last week demonstrated how one move rolls everything. On August 9th France's largest bank BNP Paribas halted withdrawals on the investment funds it said could not be fairly valued because they held subprime loans. The European Central Bank and Federal Reserve in the U.S. each added money to their own systems in response to the European banks' sudden demand for cash over the subprime loan market problems here.

The analyst at SCME Mortgage Bankers tells us that actually what you don't hear in your television news reports is that subprime loans themselves are not the problem: subprime loan delinquency rates are close to the delinquency rates on FHA/VA loans. When was the last time you heard about HUD-insured FHA loans in the media?--those low down payment loans which have been around since the Depression. Both types of loans lend to borrowers with lower FICO scores and other credit profile issues.

The difference is that the subprime loans are backed by bonds, and some hedge funds have raised capital to buy those bonds, and also borrow additional funds using that same capital, to buy more bonds through leverage. With a decrease in the value of the bonds, such as is now going on the subprime market, these hedge funds are receiving margin calls, meaning the lender wants its money. If the hedge fund cannot meet the demand, it suspends withdrawals. Some mortgage sources have paid out cash to meet the margin calls, and eventually are having to close their doors, American Home Mortgage--a strong and solid lender--being a good example. Banks which lent money to the hedge funds are now in the last few days backed up by deposits from the country's central bank, thus creating news when we read about the European Central Bank loaning $130 billion to its banks, and the Federal Reserve adding $24 billion to the U.S. banking system.

What has happened in the subprime loan market is a much larger story than a short spot on the 6 o'clock news. It's tied into our system of investing, who is regulated and is not regulated, and what happens when market factors change.

For another look at the current situation, click on this Singapore post.

Long Beach hedge fund

hedge fund credit market

credit market

The analyst at SCME Mortgage Bankers tells us that actually what you don't hear in your television news reports is that subprime loans themselves are not the problem: subprime loan delinquency rates are close to the delinquency rates on FHA/VA loans. When was the last time you heard about HUD-insured FHA loans in the media?--those low down payment loans which have been around since the Depression. Both types of loans lend to borrowers with lower FICO scores and other credit profile issues.

The difference is that the subprime loans are backed by bonds, and some hedge funds have raised capital to buy those bonds, and also borrow additional funds using that same capital, to buy more bonds through leverage. With a decrease in the value of the bonds, such as is now going on the subprime market, these hedge funds are receiving margin calls, meaning the lender wants its money. If the hedge fund cannot meet the demand, it suspends withdrawals. Some mortgage sources have paid out cash to meet the margin calls, and eventually are having to close their doors, American Home Mortgage--a strong and solid lender--being a good example. Banks which lent money to the hedge funds are now in the last few days backed up by deposits from the country's central bank, thus creating news when we read about the European Central Bank loaning $130 billion to its banks, and the Federal Reserve adding $24 billion to the U.S. banking system.

What has happened in the subprime loan market is a much larger story than a short spot on the 6 o'clock news. It's tied into our system of investing, who is regulated and is not regulated, and what happens when market factors change.

For another look at the current situation, click on this Singapore post.

Long Beachhedge fundcredit market

8/09/2007

What About Taxes on Short Pays And Foreclosures?

In case you're involved in either one of these situations, it's important to know you may be paying the IRS some money.

A "short pay" is where you were soon going into foreclosure, or you knew you were have difficulty in keeping up with your payments, and fortunately, you were able to sell before the inevitable occurred. The bank took back your loan for less than you owed on it, because you just weren't able to sell your property for more than it sold for. So if you owed $400,000 on your loan balance and the bank agreed to settle at $380,000, the bank lost $20,000 on their loan. Or, in the situation where you did go into foreclosure and the bank still lost money on their loan because they couldn't ultimately sell the property high enough to recover their loan amount, they are still faced with a money loss situation.

In either of these events, you could face a capital gain or loss or relief of debt amount for reporting on your tax return. There are many factors involved, such as how the property was held, i.e., whether or not it was your personal residence or held for resale, and what your basis was in the property, will be important information. Whether it was "recourse" or "non-recourse" debt is significant.

The important thing to know is that your tax advisor is all important in this situation. The law requires lenders to issue a 1099, but you shouldn't assume that the amount you see is the full amount of debt that you owe taxes on. This is probably not the time to do your taxes yourself, but instead seek full advice from a competent tax advisor. More information is available from the IRS.

Long Beach

A "short pay" is where you were soon going into foreclosure, or you knew you were have difficulty in keeping up with your payments, and fortunately, you were able to sell before the inevitable occurred. The bank took back your loan for less than you owed on it, because you just weren't able to sell your property for more than it sold for. So if you owed $400,000 on your loan balance and the bank agreed to settle at $380,000, the bank lost $20,000 on their loan. Or, in the situation where you did go into foreclosure and the bank still lost money on their loan because they couldn't ultimately sell the property high enough to recover their loan amount, they are still faced with a money loss situation.

In either of these events, you could face a capital gain or loss or relief of debt amount for reporting on your tax return. There are many factors involved, such as how the property was held, i.e., whether or not it was your personal residence or held for resale, and what your basis was in the property, will be important information. Whether it was "recourse" or "non-recourse" debt is significant.

The important thing to know is that your tax advisor is all important in this situation. The law requires lenders to issue a 1099, but you shouldn't assume that the amount you see is the full amount of debt that you owe taxes on. This is probably not the time to do your taxes yourself, but instead seek full advice from a competent tax advisor. More information is available from the IRS.

Long Beach

8/05/2007

How to Read Your Mortgage Documents

This is a great article from YOU Magazine specifically relating to adjustable rate mortgage documents. The links show very explanatory illustrations:

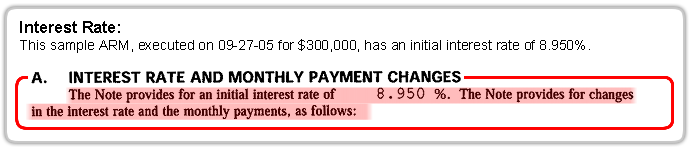

Every day you read another horror story about the subprime collapse. Most of the stories focus on the negative impact Adjustable Rate Mortgages (ARMs) will have on subprime borrowers once their interest rates reset. But what's often unreported in these news pieces is the fact that the risk extends far beyond subprime borrowers. That's right. Anyone with any ARM that is scheduled to reset may be faced with an interest rate increase of up to 2.00%-3.00%, even A-paper borrowers.

This article is not designed to scare you or add to the flood of media hype on this topic. To the contrary, our goal with this interactive article is to empower ARMs consumers with the knowledge they need to avoid becoming one of the millions of borrowers expected to foreclose in the coming years. Continue reading and you will learn how to interpret your mortgage documents, calculate your increased rate, estimate your increased monthly payment, and determine what you may need to do to avoid potential problems. We'll also show you actual loan documents and explain some of the confusing legalese that can easily lull borrowers into a false sense of security. Even better, print out this article and discuss and double-check your calculations with your mortgage professional. This will help to put your mind at ease because you'll know exactly where you stand with your mortgage.

These sample ARM documents may differ from those found in your mortgage, but they contain the basic ingredients discussed in this article and are typical of all ARMs documents, with the exception of Option ARMs (which YOU Magazine will feature in a future article).

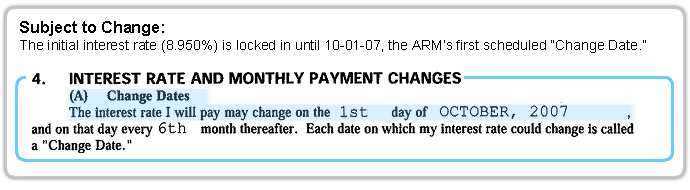

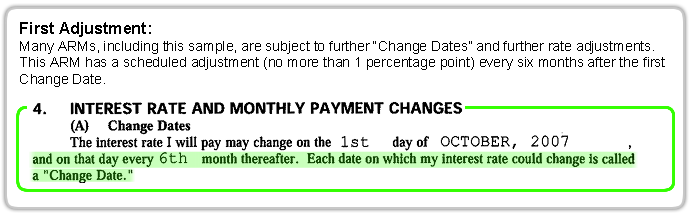

Initial interest rates on ARMs are generally locked for a predetermined period that can range anywhere from 12 months to 120 months. When the predetermined fixed-rate period of the ARM expires, the interest rate is then subject to change based on a combination of three factors.

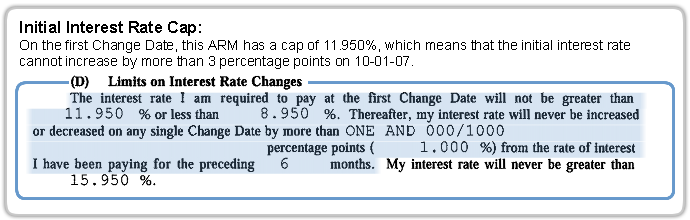

The first factor is the initial interest rate cap that was put in place at the time the loan was originated. This interest rate cap typically ranges between 2 to 5 percentage points, depending on the terms of the note. The higher cap of five points is generally in effect for loans in which the initial fixed-rate period is five, seven, or ten years. This means that if your initial interest rate was 6.00%, the maximum interest rate your loan could adjust to upon the first adjustment would be 8.00% or 11.00%. The initial interest rate cap will be in effect for 6 to 12 months before it is subject to adjust or reset. The cap on all subsequent adjustments to the interest rate should be either 1.00% or 2.00%.

For those borrowers with a subprime loan, the pain of the first adjustment will be followed with a potential increase in rates again within six months of the first adjustment.

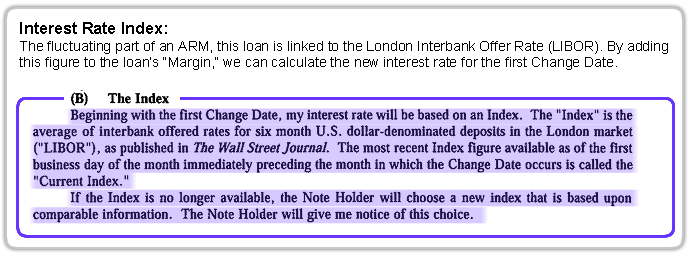

In addition to the cap, there are two components that determine the interest rate when the ARM adjusts. The first component is what is known as the interest rate index. The index is the fluctuating component of the new interest rate and is based on, or tied to, any one of several indices tracked by the Wall Street Journal, including, but not limited to: the London Interbank Offer Rate (LIBOR), U.S. Treasuries, as well as the Prime Rate.

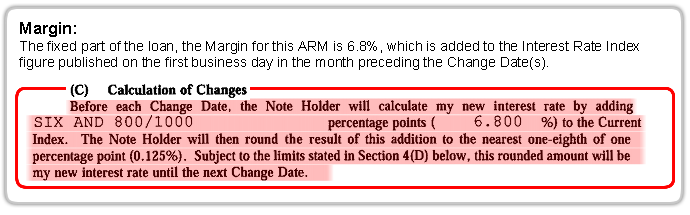

The second part of this equation is what is known as the margin. The margin is the fixed number that, when added to the index, determines the interest rate the borrower will be charged upon adjustment.

This means that, if the index tied to the mortgage is the Six Month LIBOR, which, let's say is approximately 5.38%, and the margin for a borrower was listed at 5.00, the newly adjusted interest rate could be 10.38%! If the borrower's original interest rate was 6.50%, and the loan carried a 3.00% initial interest rate cap, this loan would adjust from 6.50% to 9.50% at the first adjustment. If the index remained the same at the time of the next adjustment, the interest rate would adjust to 10.38% when the loan resets.

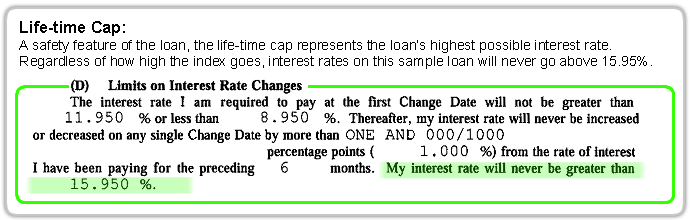

It's important to understand that, while the interest rate will never be higher than the lifetime interest rate cap, this number itself can be relatively high – the life-cap in our sample ARM is 15.95%. For borrowers who are unable to refinance due to changing circumstances, this means that rates could reach the maximum level the loan allows!

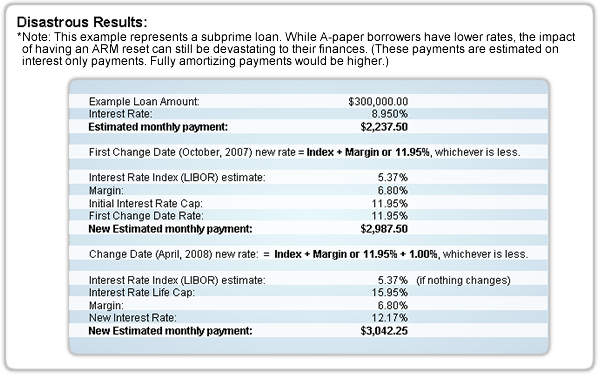

Let's apply this to a sample ARM holder and see the results. For someone with a mortgage in the amount of $300,000, the interest costs alone could increase anywhere from $6,000 to $9,000 a year. This translates into a mortgage payment increase of $500 to $750 a month just in interest. For anyone struggling to keep current on their monthly payments, such an increase could have disastrous results.

You may be wondering why anyone would take on an ARM in the first place. Despite the scenarios we've outlined here, ARMs, as a product, are not evil by design. It's true that ARMs are currently experiencing an increase in interest rates. But in a market with falling interest rates, ARMs placed at that time will experience falling rates as well, without having to refinance. Because of this feature, ARMs hold an important place in mortgage financing. In many instances, borrowers have qualified for a larger home or have been offered a lower payment for a similar amount financed because of the availability of ARMs.

Even though underwriting standards continue to tighten as a result of the subprime fallout, it does not mean that you won't qualify for an A-paper loan. Many people who may have been limited to subprime products in the past are now qualifying for Expanded Approval (EA) loans through Fannie Mae. Borrowers qualifying through EA criteria may also have the ability to qualify for Timely Payment Rewards (TPR), a program that allows for automatically reduced interest rates, without refinancing, on a 30-year fixed rate product, provided the borrower makes payments on time for a period of 24 consecutive months within the first several years of the mortgage. In most cases, borrowers with credit issues benefit more from an EA loan than from adjusting with their subprime ARM or originating a new subprime loan. Talk to your mortgage professional today about these options if you have any questions or just want more information.

Obviously, it is very important to understand the complexities of how any of these financial instruments work, as well as any potential implications the borrower might face throughout the life of the loan. Congress, many state legislatures, and the Federal Reserve are currently reviewing how mortgage companies present ARM disclosures to borrowers at the time of application to ensure borrowers better understand the mortgage process. Until then, it's up to you to protect yourself and your family. Don't get caught off guard. Pull out your ARM loan documents and use the interactive features of this article to estimate the changing cost of your ARM. If you don't like what you see, or you're still having trouble working out the numbers, make an appointment with a mortgage specialist right away.

Article also courtesy of Doug Davis at Clarion Mortgage.

Long Beach

Every day you read another horror story about the subprime collapse. Most of the stories focus on the negative impact Adjustable Rate Mortgages (ARMs) will have on subprime borrowers once their interest rates reset. But what's often unreported in these news pieces is the fact that the risk extends far beyond subprime borrowers. That's right. Anyone with any ARM that is scheduled to reset may be faced with an interest rate increase of up to 2.00%-3.00%, even A-paper borrowers.

This article is not designed to scare you or add to the flood of media hype on this topic. To the contrary, our goal with this interactive article is to empower ARMs consumers with the knowledge they need to avoid becoming one of the millions of borrowers expected to foreclose in the coming years. Continue reading and you will learn how to interpret your mortgage documents, calculate your increased rate, estimate your increased monthly payment, and determine what you may need to do to avoid potential problems. We'll also show you actual loan documents and explain some of the confusing legalese that can easily lull borrowers into a false sense of security. Even better, print out this article and discuss and double-check your calculations with your mortgage professional. This will help to put your mind at ease because you'll know exactly where you stand with your mortgage.

These sample ARM documents may differ from those found in your mortgage, but they contain the basic ingredients discussed in this article and are typical of all ARMs documents, with the exception of Option ARMs (which YOU Magazine will feature in a future article).

Initial interest rates on ARMs are generally locked for a predetermined period that can range anywhere from 12 months to 120 months. When the predetermined fixed-rate period of the ARM expires, the interest rate is then subject to change based on a combination of three factors.

{kind=link}

{kind=link}

The first factor is the initial interest rate cap that was put in place at the time the loan was originated. This interest rate cap typically ranges between 2 to 5 percentage points, depending on the terms of the note. The higher cap of five points is generally in effect for loans in which the initial fixed-rate period is five, seven, or ten years. This means that if your initial interest rate was 6.00%, the maximum interest rate your loan could adjust to upon the first adjustment would be 8.00% or 11.00%. The initial interest rate cap will be in effect for 6 to 12 months before it is subject to adjust or reset. The cap on all subsequent adjustments to the interest rate should be either 1.00% or 2.00%.

{kind=link}

For those borrowers with a subprime loan, the pain of the first adjustment will be followed with a potential increase in rates again within six months of the first adjustment.

{kind=link}

In addition to the cap, there are two components that determine the interest rate when the ARM adjusts. The first component is what is known as the interest rate index. The index is the fluctuating component of the new interest rate and is based on, or tied to, any one of several indices tracked by the Wall Street Journal, including, but not limited to: the London Interbank Offer Rate (LIBOR), U.S. Treasuries, as well as the Prime Rate.

{kind=link}

The second part of this equation is what is known as the margin. The margin is the fixed number that, when added to the index, determines the interest rate the borrower will be charged upon adjustment.

{kind=link}

This means that, if the index tied to the mortgage is the Six Month LIBOR, which, let's say is approximately 5.38%, and the margin for a borrower was listed at 5.00, the newly adjusted interest rate could be 10.38%! If the borrower's original interest rate was 6.50%, and the loan carried a 3.00% initial interest rate cap, this loan would adjust from 6.50% to 9.50% at the first adjustment. If the index remained the same at the time of the next adjustment, the interest rate would adjust to 10.38% when the loan resets.

It's important to understand that, while the interest rate will never be higher than the lifetime interest rate cap, this number itself can be relatively high – the life-cap in our sample ARM is 15.95%. For borrowers who are unable to refinance due to changing circumstances, this means that rates could reach the maximum level the loan allows!

{kind=link}

Let's apply this to a sample ARM holder and see the results. For someone with a mortgage in the amount of $300,000, the interest costs alone could increase anywhere from $6,000 to $9,000 a year. This translates into a mortgage payment increase of $500 to $750 a month just in interest. For anyone struggling to keep current on their monthly payments, such an increase could have disastrous results.

{kind=link}

You may be wondering why anyone would take on an ARM in the first place. Despite the scenarios we've outlined here, ARMs, as a product, are not evil by design. It's true that ARMs are currently experiencing an increase in interest rates. But in a market with falling interest rates, ARMs placed at that time will experience falling rates as well, without having to refinance. Because of this feature, ARMs hold an important place in mortgage financing. In many instances, borrowers have qualified for a larger home or have been offered a lower payment for a similar amount financed because of the availability of ARMs.

Even though underwriting standards continue to tighten as a result of the subprime fallout, it does not mean that you won't qualify for an A-paper loan. Many people who may have been limited to subprime products in the past are now qualifying for Expanded Approval (EA) loans through Fannie Mae. Borrowers qualifying through EA criteria may also have the ability to qualify for Timely Payment Rewards (TPR), a program that allows for automatically reduced interest rates, without refinancing, on a 30-year fixed rate product, provided the borrower makes payments on time for a period of 24 consecutive months within the first several years of the mortgage. In most cases, borrowers with credit issues benefit more from an EA loan than from adjusting with their subprime ARM or originating a new subprime loan. Talk to your mortgage professional today about these options if you have any questions or just want more information.

Obviously, it is very important to understand the complexities of how any of these financial instruments work, as well as any potential implications the borrower might face throughout the life of the loan. Congress, many state legislatures, and the Federal Reserve are currently reviewing how mortgage companies present ARM disclosures to borrowers at the time of application to ensure borrowers better understand the mortgage process. Until then, it's up to you to protect yourself and your family. Don't get caught off guard. Pull out your ARM loan documents and use the interactive features of this article to estimate the changing cost of your ARM. If you don't like what you see, or you're still having trouble working out the numbers, make an appointment with a mortgage specialist right away.

Article also courtesy of Doug Davis at Clarion Mortgage.

Long Beach

8/01/2007

Plusses and Minuses of Long Beach Condo Conversions

National homeownership by the end of the Clinton Administration supposedly rose to about 65%, the highest ever recorded. But, according to the City of Long Beach within the last few years, during that same time period, that was about how many non-owners were living in Long Beach. In other words, we were the opposite of the national picture. According to the Long Beach Business Journal, July 31, 2007 edition, the local situation may be close to reversing itself. A total of 152 conversion projects have been approved, reducing Long Beach's supply of rental homes by 2,133 since 2000.

National homeownership by the end of the Clinton Administration supposedly rose to about 65%, the highest ever recorded. But, according to the City of Long Beach within the last few years, during that same time period, that was about how many non-owners were living in Long Beach. In other words, we were the opposite of the national picture. According to the Long Beach Business Journal, July 31, 2007 edition, the local situation may be close to reversing itself. A total of 152 conversion projects have been approved, reducing Long Beach's supply of rental homes by 2,133 since 2000.No trend is perfect: The opportunity for homeownership has decreased homes available for renters. With long term population projections in the state predicting that the demand for housing will continue far into the future, there will continue to be a demand for housing for both owners and renters, and right now there's a demand for rental housing, and there may be some future restrictions on conversions to allow for a balance. The newly converted units are often smaller and priced lower--800-900 sq ft for a 2 bedroom--than the original condos. Some lenders need specific information on final conversion date and the current owner occupancy level, if any, to underwrite financing. The smaller 2-story buildings may not have elevators, however, remodeled new interiors with new appliances, for some buyers, may be a compensation for these other factors. Buyers should know that in dealing with a smaller building, they will also be a dealing with a smaller risk pool in their Association funding. The unit at 2138 E 1st St. is an upper floor 2 bd/2ba, 775 sq. ft, $238/month HOA dues, ocean view, in a historic district, and has been listed and on the market for 440 days, per today's MLS activity, in a building of 10 units where all others have now sold, list price $417,500. There are others on the market at lower prices than this one.

For a list of condo units in this area, please let me know, they're easy to e-mail.

Do tenants need some protections and acceptable and affordable housing stock, yes. Do buyers need lower-priced units and opportunity to buy in a selection of areas, yes. The story is not as completely simple as this, there are multiple effects and ramifications on each side pertaining to job impact, higher developer fees, higher rents, and units sitting on the market, but the City of Long Beach wanted more owner-occupied housing, and that is what is happening.

Subscribe to:

Posts (Atom)