4/23/2012

4/16/2012

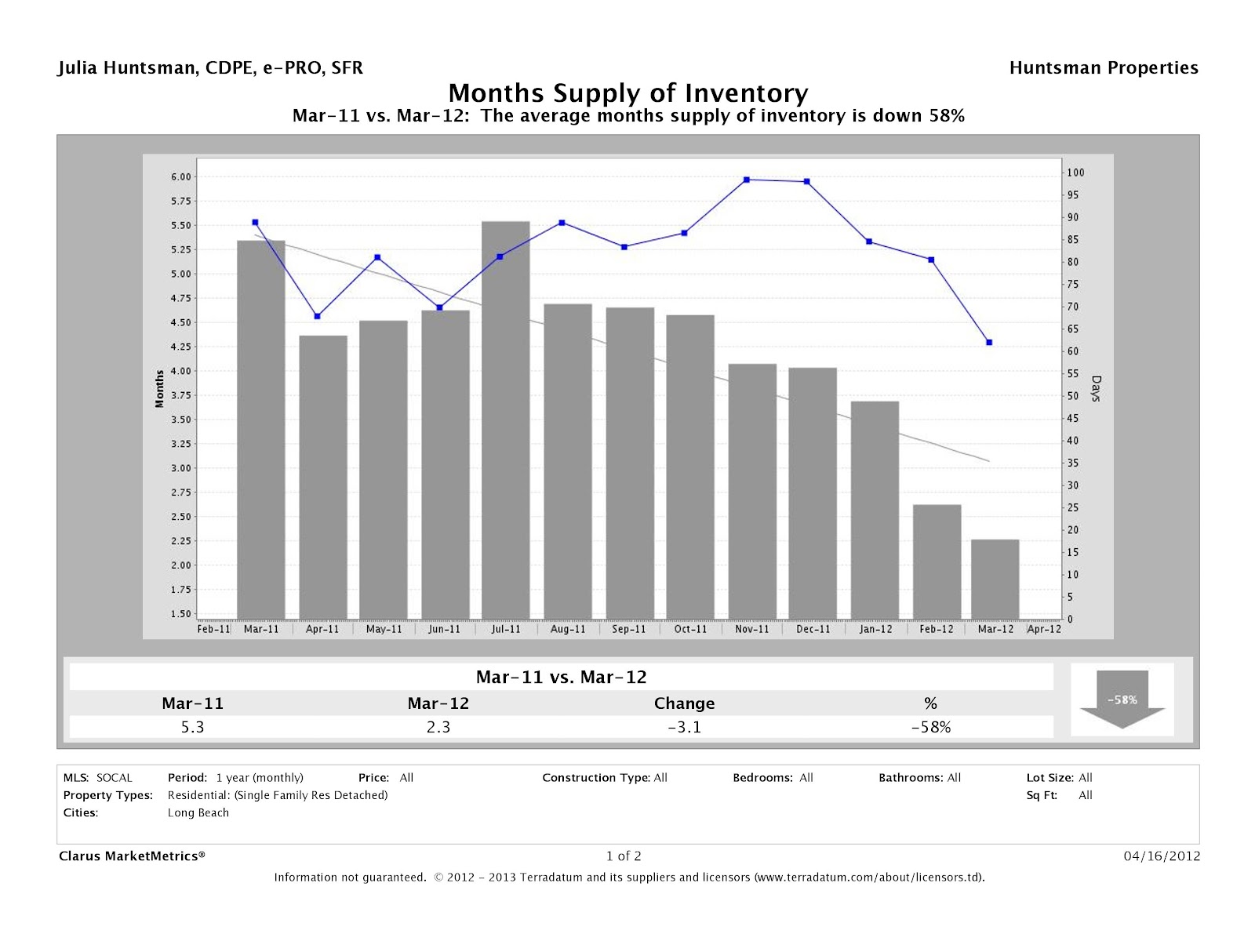

Long Beach Needs More Single Family Homes on the Market!

|

| Long Beach--two months inventory |

|

| Median price for listings is up again in Long Beach |

That means if no new listings came on the market, the current inventory would be sold in approximately 2 months at the current rate of sale.

Sellers should start contacting their real estate professional now to review their best position for selling, because the buyers, both investor and owner-occupant types, are buying!

I am available to help you as your real estate professional, just give me a call, e-mail me, or contact me through my website at www.juliahuntsman.com.

4/12/2012

California Foreclosure Study by San Francisco Assessor

This information just came in this afternoon to me from Duane Gomer, a real estate trainer active in the real estate market:

This study of 382 San Francisco homes between 2009 and 2011 was conducted by a Newport Beach-based company, and a February 2012 Orange County Register article goes into more detail here.

The San Francisco Assessor commissioned a foreclosure study during 2009 and 2011. The results are revealing and stunning to me and I’ve studied this market for decades. For example: 1 – 99% had irregularities, 2 – 84% had violation of law, 3 – 75% had issues with the assignments of the trust deeds, 4 – 84% had problems with the substitution of trustees, 5 – 59% had evidence of backdating, 6 – 45% the foreclosing party had never been assigned the loan. The Assessor’s conclusion: The California Non-Judicial Foreclosure System is “utterly broken” and needs repair.Just as further comment, the California non-judicial foreclosure law and procedures is explicitly spelled out in California code.

This study of 382 San Francisco homes between 2009 and 2011 was conducted by a Newport Beach-based company, and a February 2012 Orange County Register article goes into more detail here.

3/27/2012

Number of FHA Qualified HOAs Falling Drastically

This afternoon I was sent a list of FHA-approved condominium complexes for Long Beach. They now currently number 34, with two approvals expiring in April, leaving 32 for all of Long Beach. This is a huge reduction in number compared to a few years ago--these approvals are dropping off for two reasons: HOAs don't realize the requirements have changed or that their approval has expired and that they must renew again, or the HOA complex's financial circumstances don't currently meet FHA guidelines. But I believe many complexes fall into the first category.

If you are an HOA member, or know someone who is, think about this: If your complex is not approved for FHA-HUD loans, you greatly reduce the number of approved buyers who can bring an offer, thus probably delaying the selling date of your property.

If you are an HOA member, or know someone who is, think about this: If your complex is not approved for FHA-HUD loans, you greatly reduce the number of approved buyers who can bring an offer, thus probably delaying the selling date of your property.

If you are a buyer with an FHA approved loan (especially one being used with certain buyer assistance programs), your selection is now greatly reduced because you simply will not be able to buy in a non-FHA approved condominium complex.

Property owners, you should take active steps to look into this issue. With today's loan qualifying requirements, FHA loans are accessible for many 1st time and repeat buyers, and in the future they will become even more critical as former owners of distressed properties re-enter the market.

So you think you're going to keep living there, and it doesn't matter? What if you would like to get a reverse mortgage? They require your complex to be FHA approved.

Yes, there are lenders willing to qualify your association during escrow, but don't wait until then--it's a much longer process, and the buyer could decide to find another property.

Or the alternative is, if you're a buyer, be prepared to use a lender not of your choice, but one of the few who can give you a similar loan without needing to go FHA. In that case, call me, and I can send you to the right place.

But owners, remember, there are still FHA approvals required for reverse mortgages, therefore contacting your Board of Directors should be at the top of your agenda.

If you are a buyer with an FHA approved loan (especially one being used with certain buyer assistance programs), your selection is now greatly reduced because you simply will not be able to buy in a non-FHA approved condominium complex.

Property owners, you should take active steps to look into this issue. With today's loan qualifying requirements, FHA loans are accessible for many 1st time and repeat buyers, and in the future they will become even more critical as former owners of distressed properties re-enter the market.

So you think you're going to keep living there, and it doesn't matter? What if you would like to get a reverse mortgage? They require your complex to be FHA approved.

Yes, there are lenders willing to qualify your association during escrow, but don't wait until then--it's a much longer process, and the buyer could decide to find another property.

Or the alternative is, if you're a buyer, be prepared to use a lender not of your choice, but one of the few who can give you a similar loan without needing to go FHA. In that case, call me, and I can send you to the right place.

But owners, remember, there are still FHA approvals required for reverse mortgages, therefore contacting your Board of Directors should be at the top of your agenda.

Subscribe to:

Posts (Atom)