Every day you read another horror story about the subprime collapse. Most of the stories focus on the negative impact Adjustable Rate Mortgages (ARMs) will have on subprime borrowers once their interest rates reset. But what's often unreported in these news pieces is the fact that the risk extends far beyond subprime borrowers. That's right. Anyone with any ARM that is scheduled to reset may be faced with an interest rate increase of up to 2.00%-3.00%, even A-paper borrowers.

This article is not designed to scare you or add to the flood of media hype on this topic. To the contrary, our goal with this interactive article is to empower ARMs consumers with the knowledge they need to avoid becoming one of the millions of borrowers expected to foreclose in the coming years. Continue reading and you will learn how to interpret your mortgage documents, calculate your increased rate, estimate your increased monthly payment, and determine what you may need to do to avoid potential problems. We'll also show you actual loan documents and explain some of the confusing legalese that can easily lull borrowers into a false sense of security. Even better, print out this article and discuss and double-check your calculations with your mortgage professional. This will help to put your mind at ease because you'll know exactly where you stand with your mortgage.

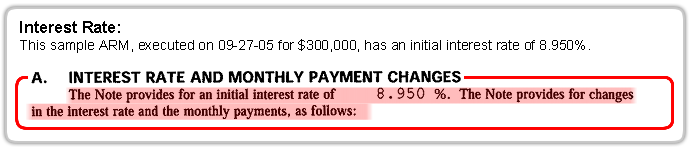

These sample ARM documents may differ from those found in your mortgage, but they contain the basic ingredients discussed in this article and are typical of all ARMs documents, with the exception of Option ARMs (which YOU Magazine will feature in a future article).

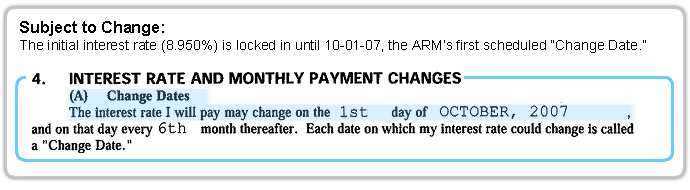

Initial interest rates on ARMs are generally locked for a predetermined period that can range anywhere from 12 months to 120 months. When the predetermined fixed-rate period of the ARM expires, the interest rate is then subject to change based on a combination of three factors.

{kind=link}

{kind=link}

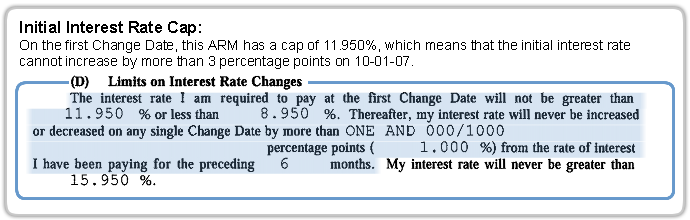

The first factor is the initial interest rate cap that was put in place at the time the loan was originated. This interest rate cap typically ranges between 2 to 5 percentage points, depending on the terms of the note. The higher cap of five points is generally in effect for loans in which the initial fixed-rate period is five, seven, or ten years. This means that if your initial interest rate was 6.00%, the maximum interest rate your loan could adjust to upon the first adjustment would be 8.00% or 11.00%. The initial interest rate cap will be in effect for 6 to 12 months before it is subject to adjust or reset. The cap on all subsequent adjustments to the interest rate should be either 1.00% or 2.00%.

{kind=link}

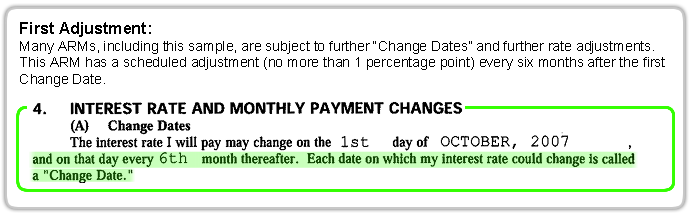

For those borrowers with a subprime loan, the pain of the first adjustment will be followed with a potential increase in rates again within six months of the first adjustment.

{kind=link}

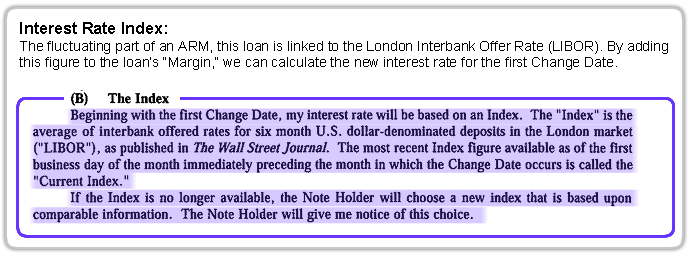

In addition to the cap, there are two components that determine the interest rate when the ARM adjusts. The first component is what is known as the interest rate index. The index is the fluctuating component of the new interest rate and is based on, or tied to, any one of several indices tracked by the Wall Street Journal, including, but not limited to: the London Interbank Offer Rate (LIBOR), U.S. Treasuries, as well as the Prime Rate.

{kind=link}

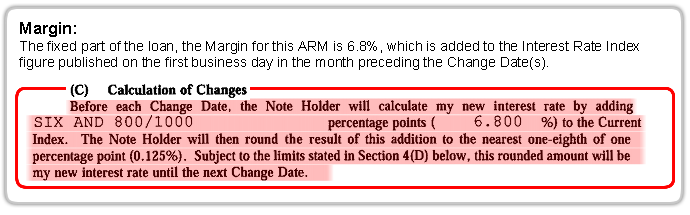

The second part of this equation is what is known as the margin. The margin is the fixed number that, when added to the index, determines the interest rate the borrower will be charged upon adjustment.

{kind=link}

This means that, if the index tied to the mortgage is the Six Month LIBOR, which, let's say is approximately 5.38%, and the margin for a borrower was listed at 5.00, the newly adjusted interest rate could be 10.38%! If the borrower's original interest rate was 6.50%, and the loan carried a 3.00% initial interest rate cap, this loan would adjust from 6.50% to 9.50% at the first adjustment. If the index remained the same at the time of the next adjustment, the interest rate would adjust to 10.38% when the loan resets.

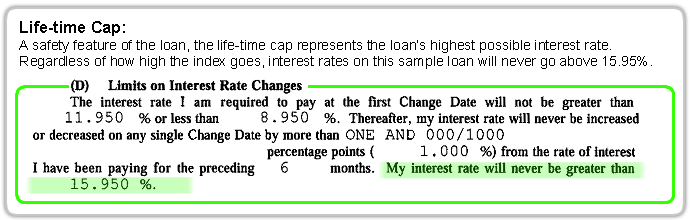

It's important to understand that, while the interest rate will never be higher than the lifetime interest rate cap, this number itself can be relatively high – the life-cap in our sample ARM is 15.95%. For borrowers who are unable to refinance due to changing circumstances, this means that rates could reach the maximum level the loan allows!

{kind=link}

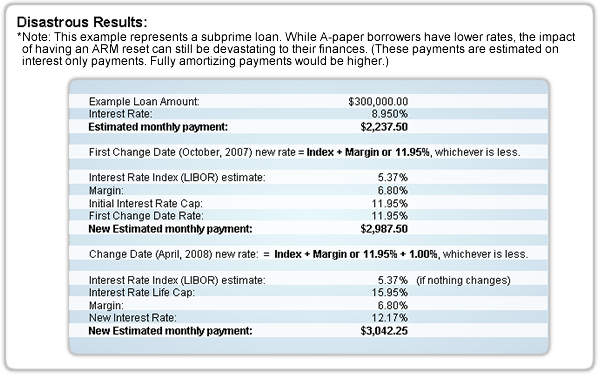

Let's apply this to a sample ARM holder and see the results. For someone with a mortgage in the amount of $300,000, the interest costs alone could increase anywhere from $6,000 to $9,000 a year. This translates into a mortgage payment increase of $500 to $750 a month just in interest. For anyone struggling to keep current on their monthly payments, such an increase could have disastrous results.

{kind=link}

You may be wondering why anyone would take on an ARM in the first place. Despite the scenarios we've outlined here, ARMs, as a product, are not evil by design. It's true that ARMs are currently experiencing an increase in interest rates. But in a market with falling interest rates, ARMs placed at that time will experience falling rates as well, without having to refinance. Because of this feature, ARMs hold an important place in mortgage financing. In many instances, borrowers have qualified for a larger home or have been offered a lower payment for a similar amount financed because of the availability of ARMs.

Even though underwriting standards continue to tighten as a result of the subprime fallout, it does not mean that you won't qualify for an A-paper loan. Many people who may have been limited to subprime products in the past are now qualifying for Expanded Approval (EA) loans through Fannie Mae. Borrowers qualifying through EA criteria may also have the ability to qualify for Timely Payment Rewards (TPR), a program that allows for automatically reduced interest rates, without refinancing, on a 30-year fixed rate product, provided the borrower makes payments on time for a period of 24 consecutive months within the first several years of the mortgage. In most cases, borrowers with credit issues benefit more from an EA loan than from adjusting with their subprime ARM or originating a new subprime loan. Talk to your mortgage professional today about these options if you have any questions or just want more information.

Obviously, it is very important to understand the complexities of how any of these financial instruments work, as well as any potential implications the borrower might face throughout the life of the loan. Congress, many state legislatures, and the Federal Reserve are currently reviewing how mortgage companies present ARM disclosures to borrowers at the time of application to ensure borrowers better understand the mortgage process. Until then, it's up to you to protect yourself and your family. Don't get caught off guard. Pull out your ARM loan documents and use the interactive features of this article to estimate the changing cost of your ARM. If you don't like what you see, or you're still having trouble working out the numbers, make an appointment with a mortgage specialist right away.

Article also courtesy of Doug Davis at Clarion Mortgage.

Long Beach

Long Beach

1 comment:

Julia, this is an important article. I'd like to post to it from my blog.

Post a Comment